These searching for to buy a home, along with present owners, may have come all through the time interval “mortgage payment lock-in influence” just lately.

It’s a relatively new phrase that occurred as a result of ultra-low mortgage fees which have been accessible in 2020-2022.

All through these years, it was totally doable to snag a 30-year mounted throughout the 2-3% fluctuate.

Truly, some lucky house owners may have even purchased their arms on a mortgage payment that begins with 1.

Proper right here’s the difficulty – now that fees have doubled, a lot of these house owners don’t want to give up their low payment. Or perhaps worse, can’t.

What Is the Mortgage Charge Lock-In Affect?

In a nutshell, the mortgage payment lock-in influence is a phenomenon the place debtors are primarily trapped of their properties attributable to very low value mortgages.

It’s not exactly a dangerous, assuming they like their property. However it has been referred to as “golden handcuffs” because of it might be significantly bittersweet.

Principally, of us with mortgage charges of curiosity locked in at 2-3% know they’ve purchased an amazing deal on their arms.

However when and as soon as they promote, they’ll lose that unbelievable payment. And worse however, they’ll must deal with a significantly better mortgage payment within the occasion that they buy one different dwelling and finance it.

Truly the one answer to stay away from this case is to advertise and rent, or promote and buy a home with cash.

Each different state of affairs primarily results in a doubling of the borrower’s fee of curiosity, from that 2-3% fluctuate to 6%+.

Not solely is that this a difficult capsule to swallow, it moreover presents affordability challenges. Notably since dwelling prices haven’t come down all that quite a bit.

Keep in mind, there isn’t a dangerous correlation between dwelling prices and mortgage fees. Every can rise collectively, or fall collectively.

Though given the steep enhance in mortgage fees just lately, there was clearly some downward pressure on dwelling prices, notably in areas of the nation that observed enormous constructive points.

Nonetheless, attributable to this payment lock-in, present dwelling present is large restricted and has saved dwelling prices elevated.

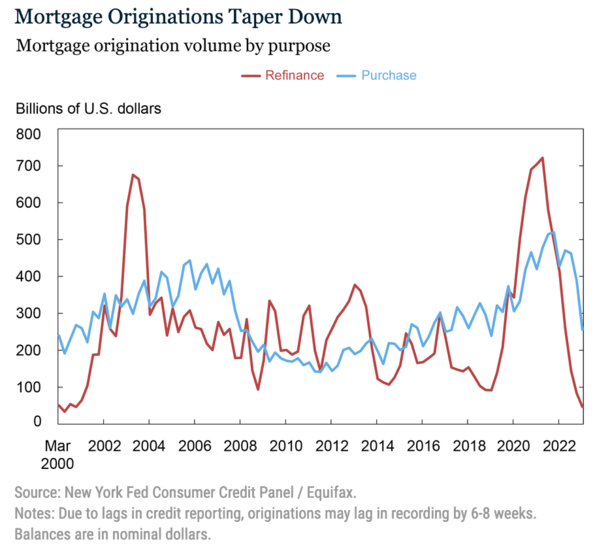

Mortgage Prices Doubled After the Refi Improve

As well-known, the 30-year mounted was priced throughout the 2-3% fluctuate a few years previously. It formally hit its lowest stage on file by the week ending January seventh, 2021, in accordance with Freddie Mac.

For the time being, you may get a 30-year mounted mortgage for 2.65%, and really even lower for many who paid low value elements. Or simply shopped spherical for the right deal.

And that’s exactly what many homeowners did. The so-called “Nice Pandemic Mortgage Refinance Growth” resulted in about 14 million new mortgages between the second quarter of 2020 and the fourth quarter of 2021.

Per the Federal Reserve Monetary establishment of New York, about 5 million debtors extracted a whole of $430 billion in dwelling equity by their refinance. These are known as cash out refinances.

One different 9 million refinanced their loans with out equity extraction and lowered their month-to-month funds throughout the course of. That is named a payment and time interval refinance.

It resulted in a staggering $24 billion together lowered annual housing costs. And keep in mind, that could be for the next three a few years on these 30-year mounted mortgages.

And certain, mounted, which implies the speed of curiosity doesn’t change, it doesn’t matter what happens with mortgages throughout the meantime.

Speaking of, the going payment on a 30-year mounted is now nearer to 6.5%, per Freddie Mac.

Can Current Homeowners Afford to Switch?

Now shopping for and promoting in a mortgage priced at 2-3% for one above 6% is clearly unfavorable, notably if the home worth doesn’t change quite a bit.

This makes a lateral switch disadvantageous, and a move-up purchase unlikely.

Shifting from one like dwelling to a unique merely isn’t cost-effective. Let’s take into consideration an occasion.

Say you purchased a home in 2021 for $500,000, put down 20%, and obtained a 30-year mounted at 2.75%.

That locations the month-to-month principal and curiosity payment at $1,632.96. What a deal!

Now take into consideration you develop tired of your own home, or simply want to switch for irrespective of motive. A home you need goes for $475,000. Prices received right here down barely bit.

You set down 20% and wind up with a mortgage amount of $380,000, nevertheless the mortgage payment is now 6.5%. Ouch!

That locations the month-to-month principal and curiosity payment at $2,401.86. What a drag!

Your mortgage payment merely elevated about $770, or 47%. Positive, you’re finding out that correct. So not solely is it an infinite deterrent to maneuver, it’s moreover doubtlessly unaffordable for some (or many).

This explains why a lot of at current’s house owners are primarily locked-in to their present properties.

Each because of it makes no financial sense to maneuver, or because of it’s not even moderately priced to take motion.

Truly, some house owners possibly couldn’t get licensed for a home mortgage at at current’s quite a bit better fees.

Nonetheless Can’t the Mortgage Charge Lock-In Affect End If Prices Come Down?

People who don’t buy into this entire mortgage payment lock-in influence argue that life happens. People will switch for numerous causes, irrespective of their low mortgage payment.

Whereas that’s true, it’s unclear what variety of will switch for these causes. It could be a fairly small proportion of the final pie.

Moreover they declare that over time, there’s a diminishing value to the low-rate mortgage. In any case, each time you make a month-to-month mortgage payment, you could possibly have one a lot much less at your disposal.

Nonetheless take into account that a 30-year mounted comes with 360 month-to-month funds. So it’ll take a extremely very very long time for that state of affairs to play out.

What may put an end to the mortgage payment lock-in influence is lower mortgage fees. They don’t primarily have to be 2-3% as soon as extra, merely one factor throughout the ballpark.

So perhaps 30-year mounted fees once more throughout the 4% fluctuate would do it. It’d be additional palatable for a home proprietor to swap a payment of three% for a payment of 4.5%. And further moderately priced too!

You could argue that falling dwelling prices would entice people to maneuver, nevertheless they’d moreover want to advertise throughout the course of. And it’s unclear within the occasion that they’d want to take a haircut and lose their low payment.

What may be additional probably might be renting out their dwelling and purchasing for one different if which have been to happen.

This explains why house owners may be preserving their mortgages for a extremely very very long time. And why being locked in can actually be a wonderful issue.